The Boom and What Comes Next.

By Ed Sullivan

In the middle of a difficult period for housing and traditional nonresidential building, one sector has emerged as a force powerful enough to alter growth in regional cement markets. Growth in the construction of data centers in recent years has been extremely strong and does not appear to be slowing down anytime soon. Understanding where this boom is headed, and what forces will eventually govern its pace, has become one of the more important analytical issues facing the construction outlook over the next five years. This article gives TSR’s view and how it impacts overall construction activity and cement consumption.

Purpose-Built: The Unique Requirements of Data Center Construction

The data center construction stems from the needs of artificial intelligence (AI). AI applications, in all their forms require vast amounts of computing power. That computing power lives in data centers. Data center buildings have four unique needs that no ordinary building can provide: city-scale power, continuous precision cooling, floors engineered for extraordinary structural loads, and massive fiber connectivity. Typically, this combination requires new facility construction.

Not all data centers are the same, and the differences matter enormously for understanding the construction boom under way today. At one end of the spectrum are hyperscale campuses. These are massive, multi-structure complexes built on hundreds of acres and owned by the major players in AI (Amazon, Microsoft, Google, Meta, etc.). They consume as much electricity as a small city. At the other end of the spectrum are small edge facilities that are often retrofitted to existing buildings.

Hyperscale Campus – Hyperscale campuses account for roughly 150 to 200 locations across the United States but represent nearly two-thirds of total data center construction spending. These building types are enormous, demanding heavily reinforced concrete to support server racks that can weigh 10 to 15 times more than normal office equipment. In addition, the concrete pads and enclosures for transformer yards and backup generator systems are required to support energy and cooling needs. And with energy consumption comes heat, requiring cooling towers. Add atop all this the campus roadways, drainage systems and site infrastructure that a facility of this scale requires, and you get a massive consumer of cement/concrete. While each campus is different, a single hyperscale campus of 500 megawatts can cost $5-$10 billion and consume approximately 150,000 to 300,000 metric tons of cement over its construction cycle. A large multi-phase campus development can exceed that range considerably.

Colocation Facilities – While the hyperscale campuses grab the headlines, not all data center activity is this large. Colocation data centers house servers for multiple corporate tenants under one roof — hence “colocation.” The owner provides the space, power, cooling and security. These facilities are smaller than hyperscale campuses and structurally lighter, but they exist in virtually every major metropolitan market in the country. There are approximately 1,200 to 1,500 of these operating across the country, representing roughly 25 to 30% of construction spending.

The smaller footprint, floor loading requirements, and the on-site power infrastructure requires significantly less than a hyperscaler — requiring less cement/concrete. A typical newly constructed colocation facility in the 20- to 50-megawatt range consumes roughly 10,000 to 25,000 metric tons of cement during construction. Not all colocation is new construction — converted warehouses serve part of the market. But the weight of server racks generates the need for concrete reinforced structures as part of the facility’s retrofit.

Edge and Enterprise Facilities – These are small local computing centers within existing buildings. These facilities generate minimal new construction activity and negligible cement consumption.

Extraordinary Returns Drive Extraordinary Investment – In 2000, the United States had roughly 300 data centers, concentrated in a few metropolitan corridors — Northern Virginia, Silicon Valley, the New York metropolitan area. They were utilitarian facilities housing corporate servers and early internet infrastructure. Their construction footprint was modest, their cement consumption negligible. Growth in data center construction was steady and modest through the early 2020s. The boom in data center construction has a very specific starting point — late 2022, when the public launch of generative AI made the computing infrastructure requirement suddenly and dramatically visible to the entire investment community. What had been gradual became explosive almost overnight.

Artificial intelligence is software that learns, reasons and makes decisions, and promises productivity gains, new products, profits and structural economic change of a magnitude not seen since the industrial revolution. Delivering on that promise requires dramatic increases in computing power. It requires data centers. Developers building data centers today are targeting returns of 20% to 30% on their investment. That is an extraordinary return by any standard. It explains everything about why capital is flowing in at the current pace and why data center construction is booming.

Today, data centers bear little resemblance to their 2000 counterparts. Today’s hyperscale campus — the kind being built by Amazon, Microsoft, Google and Meta — is a multi-building, heavily engineered complex consuming 500 megawatts or more of power, sitting on hundreds of acres, and requiring the kind of structural foundation work that rivals a major industrial facility. These are not server closets. They are among the most capital-intensive construction projects in the American economy.

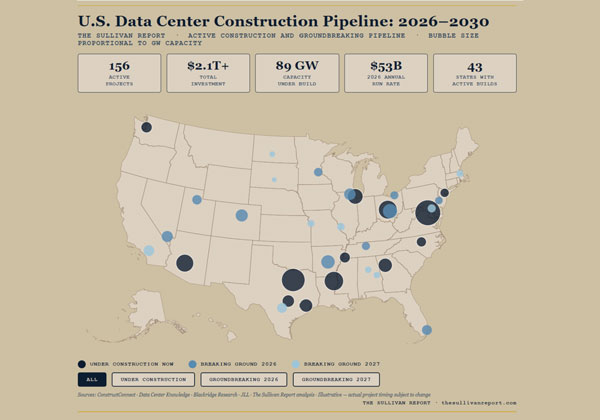

The numbers are staggering by any measure of construction activity. U.S. data center construction spending stood at $27 billion in 2024. It reached an estimated $41 billion in 2025, a 52% increase in a single year. The annualized run rate entering 2026 is approaching $53 billion. To put that trajectory in context, year-to-date spending through October 2025 was more than double the comparable figure from 2024 and nearly eight times the level recorded in the first 10 months of 2023. In July 2025 alone, a single month of construction starts totaled $14 billion — more than the entire first half of that year. This is not normal growth. This is a structural transformation of the American construction landscape.

This is not a regional phenomenon confined to a handful of markets. It is a national buildout of digital infrastructure at a pace and scale with few historical precedents. While aggressive data center construction has materialized in northern Virginia, Phoenix, Dallas, Atlanta, Chicago, Columbus and Seattle — the geographic picture is broader and more consequential for regional cement demand than the headline markets suggest. Meaningful data center construction activity is now present in 43 of the 48 continental states. The five states with little to no activity are largely rural states with limited power grid infrastructure.

The buildout of hyperscale infrastructure has followed power availability, land cost and fiber connectivity into markets that were barely on the map a decade ago. Central Ohio has emerged as one of the fastest-growing data center markets in the country, driven by favorable power infrastructure and proximity to Midwest population centers. The Carolinas, Tennessee, and the broader Southeast are absorbing significant colocation investment. The Mountain West — Idaho, Utah, Wyoming — is seeing edge infrastructure expand alongside its energy resources. This geographic diffusion matters enormously. It means data center demand is showing up in state-level consumption figures across the country, often in markets where other nonresidential and residential construction drivers have been weak.

The Boom Is Building Its Own Ceiling

This dramatic growth does not show signs of abating anytime soon. Recent spending data from the U.S. Census shows first quarter growth running 33% above 2025’s robust levels. Indeed, growth is so strong that construction worker shortages are threatening to slow down the construction of facilities and at the same time prolong its growth.

At its foundation, the driver behind data center construction is profit. As long as developers building data centers today earn very large returns on their investments, construction will remain robust. Chasing the certainty of robust returns, capital flows into further investments without hesitation. Currently, the demand for AI computing capacity is vast, and the supply of facilities to house it is constrained. This tends to keep the profitability in building data centers elevated — and ensures its near-term growth momentum.

The forces that will eventually slow data center construction are not coming from outside the boom. They are being created by the boom itself. Every new data center built makes energy more expensive for the next one. Every new campus started makes skilled labor harder to find for the one after it. The boom is quietly building its own ceiling.

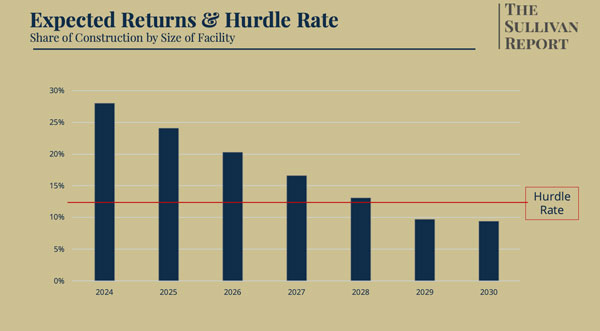

While it doesn’t seem like it is in the near-term cards, eventually the robust returns on data centers will ease. When those returns begin to ease, so will the rate of growth in data center construction. The key issue is not whether data center investment returns will eventually moderate, but what forces will govern the timing and pace of that moderation. There are three principal factors that could bring about the moderation in data center construction growth. Consider the following:

Computing Price Erosion: As more data center capacity comes online, the price of AI computing is expected to ease and is a normal feature of maturing technology markets. This is already happening; the price of running AI applications has declined dramatically over the past three years as supply has grown. That trend will continue, gradually eroding the revenue that each megawatt of deployed capacity generates. By this logic, the return on a data center built in 2030 will be lower than the return on one built in 2020, all else equal.

Energy Cost Escalation: The computing that goes on within a data center requires a lot of power. Energy costs are rising across the entire economy driven by electrification, reshoring, population growth and surging industrial demand — and data centers must compete for that constrained grid alongside every other major consumer. In the near term, this collective demand growth substantially outpaces the expected expansion of supply.

Data centers are key contributors to this growth. Analysts estimate that 4.1% of total energy demand was accrued to data centers in 2025. By 2027, that share is expected to rise to 8.5% and reach 17% by 2030. In northern Virginia, it is expected to account for as much as 57% of total electricity demand in the region. And each subsequent data center project pays more for grid upgrades, for power purchase agreements, and for backup generation. This cost escalation is driven by each of the factors cited above. The data center boom is a significant cause of this escalation and it intensifies as the buildout accelerates.

Labor Scarcity: Data center construction is extraordinarily intensive in its use of licensed electricians and specialized trades. Many of these trades are nearing retirement. The expected new entrants to these trades are not expected to offset this supply drag. Labor costs among these trades are rising and it is likely that scarcity will accelerate the near-term premium for these workers.

While there may be other factors, these forces work simultaneously to either reduce revenue or increase the costs associated with data centers. The profit margin on the construction of data centers at some point will gradually decline, reducing the investment incentive. This gradual erosion in expected data center margins is expected to cause a deceleration in the growth of their construction.

The full pipeline of announced hyperscaler commitments suggests continued strong demand through at least 2028. Beyond that, the pipeline becomes somewhat more uncertain, and the standing and future commitments will be increasingly dictated by the trajectory of computing price decay, and energy and labor cost escalation.

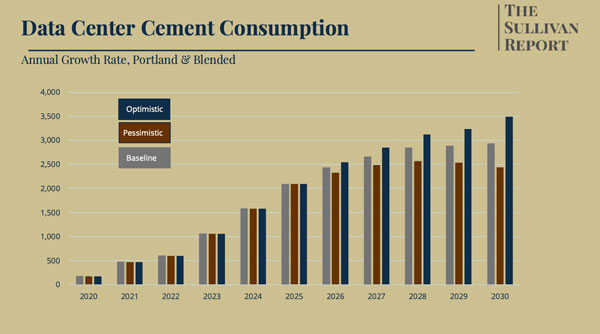

Under our most optimistic assumptions, strong growth in data center construction spending continues through 2032 before meaningful deceleration sets in. Under our most conservative assumptions, the pace of new commitments begins to moderate around 2030 to 2031, with construction spending plateauing shortly thereafter. According to this analysis, even under the most conservative assumptions, the data center construction boom has at minimum four years of sustained, robust growth ahead of it.

What This Means for Cement and Why the Numbers Are Bigger Than Some Report

Amid difficult conditions impacting residential and most traditional nonresidential sectors, data center construction grew 32.3% in 2025 — reaching more than 2 million metric tons of cement consumption. The first-quarter 2026 data suggests the rate is accelerating. Keep in mind, reported shortages of skilled workers may have restrained some construction activity, strengthening the case for future data center construction.

Our estimates on historical data center cement consumption assess the inventory of projects under construction, the planned completion dates, the stage of production (cement and concrete consumption is greatest in early stages of construction), inclusion of infrastructure, plant sizes, and carefully estimated cement intensities by tier of construction (large 4 GW campuses versus edge data centers). We make sure that we measure only construction activity and weed out expensive equipment spending that is often included in plant spending (70%) estimates (if this is not undertaken, cement intensities will underestimate cement consumption).

The near-term outlook for data center construction is straightforward: robust growth continues. The pipeline of announced projects is deep, the capital commitments are made, and the construction lags involved in large campus development mean that activity already in motion will continue generating cement demand for years regardless of what happens to the investment climate. Through at least 2028, the trajectory is essentially locked in.

Beyond 2028, however, the forces described earlier regarding data center construction begin to assert themselves. Computing revenues per megawatt of deployed capacity are expected to gradually ease as supply grows. Energy costs will likely continue to rise as the grid strains under unprecedented demand. Construction labor will likely remain scarce and expensive. Taken together, these forces compress the return on data center investment.

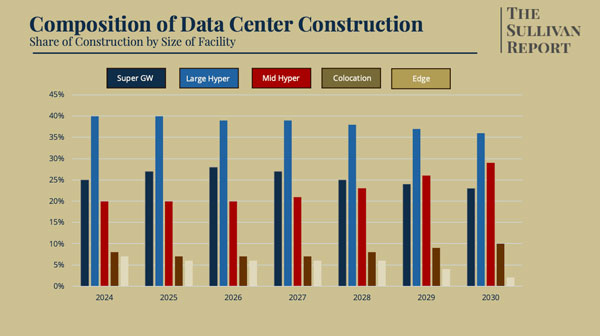

At some point, the expected return on the next data center campus falls below the threshold that justifies breaking ground on large-scale investments. New commitments to these large investments are expected to slow. Due to lower costs and investment risks, data center construction is expected to shift toward smaller projects. At some point, the construction pipeline, which had been continuously replenished, begins to drain and overall data center construction declines. Our base case places that inflection in the 2030 to 2031 window. Even under the most conservative assumptions, the boom has at minimum four years of sustained growth remaining.

It is important to note that cement consumption will be determined by not only the amount of data center construction activity, but also by the cement intensity associated with the type of data centers constructed. As the expected returns for data centers ease, capital is expected to migrate toward smaller, lower-risk investments. This implies a shift from hyperscaler construction, which requires considerable cement/concrete to build, to colocation facilities and edge facilities, which require significantly less cement/concrete to construct. For cement consumption, the easing in expected returns on data center investments not only results in less construction, but the construction that does result is generally less cement intensive.

Our base case projects data center cement consumption reaching nearly 3 million metric tons by 2030. Under our most optimistic assumptions that figure approaches 3.3 million metric tons. Under our most conservative assumptions, consumption peaks near 2.6 million metric tons around 2028 before beginning a gradual decline as both spending growth and cement intensity moderate simultaneously. Keep in mind, as the easement in data center construction materializes in the next decade, construction of utilities and power generation facilities that are required to support the operation of data centers are expected to build significant momentum.

Conclusion

Data center construction has become one of the most consequential drivers of U.S. cement demand — and one of the least precisely measured. Our analysis suggests the sector is larger, more geographically dispersed, and more analytically complex than some published estimates have captured.

The boom is real, the runway is substantial and the forces that will eventually govern its pace are already visible to those looking carefully enough. For cement producers and construction executives navigating this environment, the national picture presented here is the starting point. For those whose markets are being shaped by this buildout in specific states and regions, that same analytical framework presented in this report is applied at the state and regional level and presented in our state/regional forecasts.

Ed Sullivan has been an economist, author and public speaker for more than 30 years. Before launching his current company, The Sullivan Report, he served as a chief economist and senior vice president of market intelligence at Portland Cement Association (now ACA) for more than two decades. For more information, go to www.thesullivanreport.com.